- The European dental software market is undergoing a significant digital transformation, with rapid adoption of innovative solutions reshaping clinical workflows, patient management, and diagnostic capabilities across the continent. Driven by an aging population, increasing prevalence of dental disorders, and a strong push for digital health, the market is poised for substantial growth in the coming years.

Europe's Digital Dentistry Boom: Key Drivers and Market Outlook

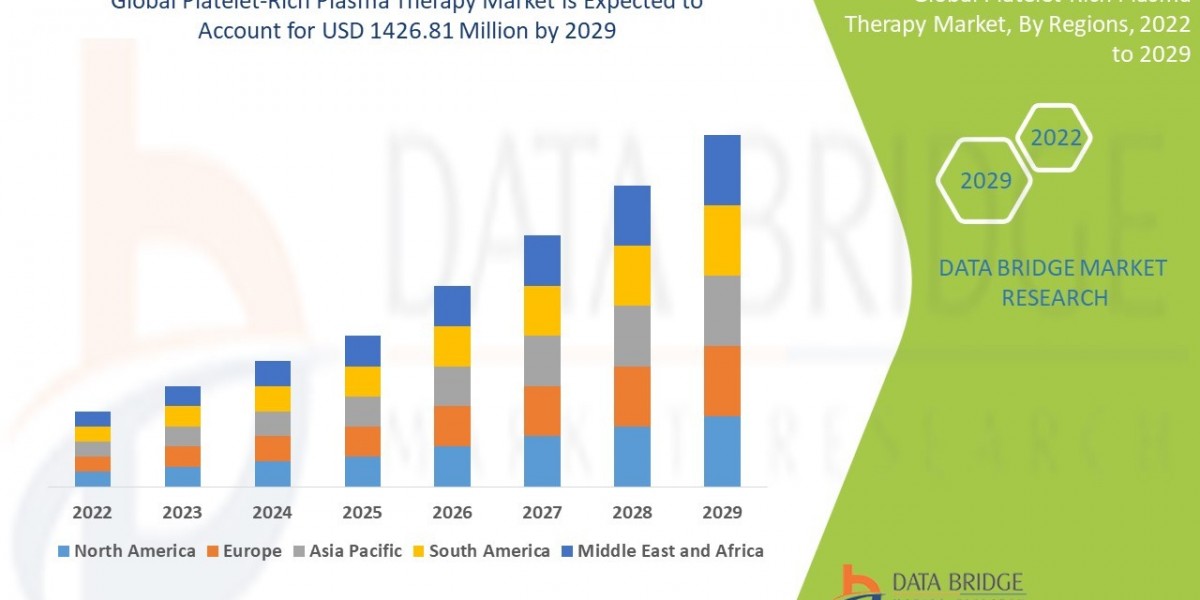

Europe holds a prominent position in the global dental market, projected to grow at an impressive CAGR of 8.0% during the forecast period (2023-2030). The overall dental software market is experiencing substantial growth, with projections indicating a global valuation of USD 6,152.70 million by 2031, up from USD 2,870.09 million in 2023, exhibiting a CAGR of 10.1%. This robust expansion in Europe is fueled by several critical factors:

- Aging Population and Rising Dental Disorders: With over 20% of Europe's population expected to be aged 65 or older by 2030, and oral health issues affecting over 50% of Europeans, there's a heightened demand for efficient and specialized dental care. Dental software plays a crucial role in managing complex treatment plans and streamlining operations for a larger patient load.

- Increasing Adoption of Digital Health Solutions: Government initiatives, such as the European Health Data Space, are promoting interoperable systems to enhance data sharing and operational efficiency. Over 70% of healthcare providers in Europe now utilize digital tools for administrative and clinical tasks, reflecting a broader trend towards digitization in healthcare.

- Technological Advancements: Rapid advancements in areas like cloud computing, artificial intelligence (AI), and advanced imaging methods are significantly improving the capabilities of dental software. These innovations facilitate early-stage diagnosis, precise treatment planning, and enhanced patient engagement.

- Shift Towards Paperless Practices: The move to digital alternatives for patient data, treatment plans, and other crucial documents is driven by the need for effective information management, reduced physical storage, and easier access to patient records.

Within Europe, the dental practice management software market alone is expected to reach a projected revenue of US$ 1,434.9 million by 2030, growing at a CAGR of 10% from 2024. Cloud-based solutions are emerging as the fastest-growing deployment mode due to their scalability, accessibility, and reduced IT costs.

Innovations and AI Integration Shaping the Future

The European dental software landscape is a hub of innovation, with key players and emerging startups focusing on advanced features and AI-powered solutions.

- AI in Diagnostics and Treatment Planning: AI algorithms are being integrated into dental software for tasks ranging from analyzing face structures for smile simulations (e.g., SmileAI) to identifying diseases in dental X-rays. Companies like Pearl, a global leader in dental AI solutions, are expanding their presence in Europe, offering AI-powered tools for disease detection and insurance eligibility verification.

- Enhanced Imaging Solutions: Dental imaging software in Europe is projected to reach US$ 613.4 million by 2030, with extraoral imaging being the fastest-growing segment. Companies like Vatech are continuously developing cutting-edge X-ray imaging solutions with features like low doses and advanced 3D capabilities.

- 3D Printing Integration: Partnerships like Stratasys's collaborations in Spain and Germany are expanding the availability of comprehensive dental 3D printing solutions, including full-color digital dentures. This integration with software allows for streamlined workflows, reduced labor time, and cost savings in dental laboratories.

- Patient Engagement and Communication: Software solutions are increasingly focusing on improving patient communication, appointment scheduling, and patient record management, enhancing the overall patient experience.

Regulatory Landscape and Challenges

The European medical device regulatory framework, specifically the EU 2017/745 or Medical Device Regulation (MDR), significantly impacts dental software manufacturers. This regulation, applicable since May 2021, aims to ensure a high level of safety and health while supporting innovation. All new or updated products must comply with MDR, which includes stringent requirements for documentation, laboratory tests, and user testing to obtain the CE mark for commercialization across EU member states.

Despite the rapid growth and technological advancements, the market faces challenges such as high initial costs of implementing dental software, data security concerns (especially with cloud-based solutions), and the need for greater interoperability between different systems. However, ongoing public and private investments in R&D and the increasing number of dental clinics across Europe are expected to overcome these hurdles, fostering continued market growth.

Key Players Driving the European Market

Major companies like Henry Schein Inc., Carestream Dental, LLC, Patterson Dental Supply, Inc., and Epic Systems Corporation are significant players in the European dental software market. Their continuous investment in research and development, strategic partnerships, and focus on integrating advanced technologies are shaping the competitive landscape. As digital dentistry continues to evolve, Europe is firmly positioned at the forefront of this transformation, promising more efficient, accurate, and patient-centric dental care for its citizens.