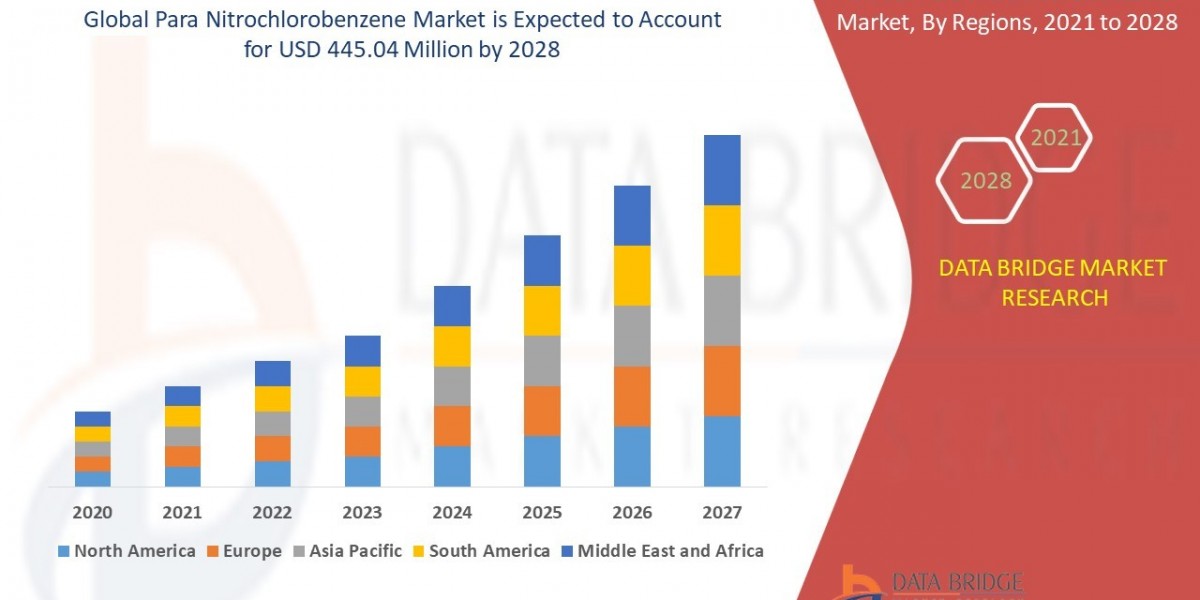

The Vertical Leap: Exploring the 3D Semiconductor Packaging market share

The semiconductor industry, the bedrock of modern technology, is constantly pushing the boundaries of what's possible. As traditional 2D scaling of transistors faces fundamental physical limitations, a new paradigm is emerging to meet the relentless demand for higher performance, lower power consumption, and smaller footprints: 3D semiconductor packaging market share. This innovative approach involves stacking multiple integrated circuits (ICs) vertically, rather than laying them out side-by-side, creating a dense and highly interconnected system. The 3D semiconductor packaging market share is currently experiencing significant growth and is poised for even greater expansion in the coming years.

At its core, 3D packaging revolutionizes how chips are designed and integrated. By stacking dies, manufacturers can achieve shorter interconnect lengths, leading to faster data transfer speeds, reduced power loss, and significantly higher bandwidth. This vertical integration allows for heterogeneous integration, where different types of components – such as logic, memory, and sensors – can be combined in a single package, optimizing performance for specific applications. Think of it as moving from a sprawling bungalow to a high-rise skyscraper; more functionality packed into a smaller, more efficient space.

Several key technologies underpin the 3D semiconductor packaging market share. Through-Silicon Vias (TSVs) are arguably the most crucial. These tiny vertical electrical connections pass directly through the silicon wafer, enabling communication between stacked dies. TSVs offer superior electrical performance compared to traditional wire bonds and provide the necessary pathways for high-density interconnections. Other important technologies include wafer bonding, which physically joins the wafers or dies together, and micro-bumping, which creates the electrical contacts between layers. Advancements in these areas are continuously driving the capabilities and cost-effectiveness of 3D packaging solutions.

The applications for 3D semiconductor packaging are vast and expanding rapidly. High-performance computing (HPC) and data centers are major drivers, where the need for immense processing power and efficient memory access is paramount. Graphics processing units (GPUs) and artificial intelligence (AI) accelerators, which handle vast amounts of data in parallel, particularly benefit from the bandwidth and low latency offered by 3D stacked memory like High Bandwidth Memory (HBM). In the consumer electronics sector, the push for smaller, more powerful devices like smartphones and wearables is also fueling adoption. Furthermore, the automotive industry, with its growing demand for advanced driver-assistance systems (ADAS) and autonomous driving capabilities, is increasingly incorporating 3D-packaged sensors and processors for enhanced performance and reliability.

The growth trajectory of the 3D semiconductor packaging market share is robust, propelled by several factors. The "More than Moore" era, where innovation extends beyond simply shrinking transistor sizes, is creating a fertile ground for advanced packaging solutions. The proliferation of AI and machine learning across various industries necessitates the specialized architectures that 3D packaging can enable. Moreover, the escalating demand for edge computing, where processing power is moved closer to the data source, further underscores the need for compact, high-performance packages. The ongoing drive for energy efficiency in electronic devices also favors 3D integration due to its inherent power benefits.

Despite its immense potential, the 3D semiconductor packaging market share also faces challenges. The complexity of the manufacturing process, involving precise alignment and bonding of multiple thin wafers, requires significant capital investment and specialized expertise. Yield management, ensuring a high percentage of defect-free packages, is another critical aspect. Thermal management is also a concern, as stacking components can lead to increased heat density, necessitating innovative cooling solutions. Standardization across the industry is another area that requires attention to facilitate broader adoption and interoperability.

Looking ahead, the future of the 3D semiconductor packaging market share appears exceedingly bright. Continuous advancements in materials science, manufacturing techniques, and thermal management solutions will further enhance its capabilities. The integration of advanced testing and inspection methodologies will be crucial for maintaining high yields. As the semiconductor industry continues its evolution, 3D packaging is set to play an increasingly vital role, enabling the next generation of electronics that are faster, smaller, more powerful, and more energy-efficient, ultimately shaping the technological landscape for decades to come.

Related Reports:

Brazil Service Robotics market share

US Building Automation System market share

UK Building Automation System market share